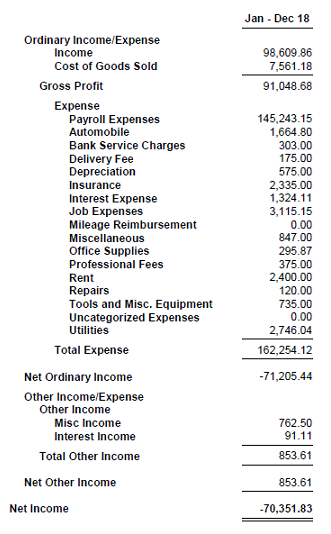

What is a Profit & Loss Statement, and What Do I Use It For?

Put simply, a Profit & Loss Statement (also called P&L or Income Statement) is the report that summarizes your business income and expenses. There are three types of accounts that go on your P&L: Income, Cost of Goods  Sold (or COGS), and Expenses.

Sold (or COGS), and Expenses.

Income includes:

- Money earned for selling goods or services

- Interest earned or other non-sales income

COGS includes:

- Cost of product you sell

- Labor to produce said products

Expenses include:

- Money spent on operations such as rent, office supplies, etc.

- Expenses do not include asset purchases such as machinery, vehicles, etc.

The P&L tells you the net income (or loss) of your business. But what else is it used for? Mainly, taxes. The bottom line on the P&L is the basis for your tax bill to Uncle Sam, so you want to ensure its accuracy.

Being self-employed, you may not have W-2’s to present in application for things such as loans, insurance, or investments, so the P&L tells the potential creditors/investors what your income looks like.

Reviewing the P&L is an important procedure for the business owner as well. For example, do you have a busy season? Analyzing the performance during the whole year can help you budget for slow season.